In September 1998, Bei Cai Caijing imported a first-generation LCD panel production line from DTI (a joint venture between Toshiba and IBM). As there is no core technology, the company cannot continue to develop. In 2003, Chinese companies reintroduce LCD panel production lines. However, due to patent fees, the prices of products were not competitive, and this attempt ended in failure. By 2008, customs data showed that in 2008 China's panel industry trade deficit reached the record high of 148.796 billion yuan (calculated at the end of 2008). China's demand for LCD panels has been completely dependent on imports for a long time. Even China's annual import material consumption ranking is second only to oil, iron ore, and chips.

Rising history from trade deficit to the world's top

Apparently ten years ago, Chinese panel companies were basically in a state of “negligence and whiteness,†and panel demand basically relied on imports. However, by 2018, China's panel industry has made amazing changes in just a decade. According to statistics from IHS (Data Statistics and Analysis Corporation), China is expected to become the world's largest flat panel display production region in 2018, accounting for 35% of the global market.

Not only does it have an advantage in scale, the technological pace of Chinese panel companies has gradually begun to keep pace with the international rhythm. BOE has a 6th-generation flexible AMOLED production line in Mianyang, and Huaxing Photoelectric's 6th-generation flexible LTPS-AMOLED project and 11th-generation TFT-LCD and AMOLED projects are also under construction. In addition, Visionox and Harmonix have made great advances on AMOLED and flexible OLEDs.

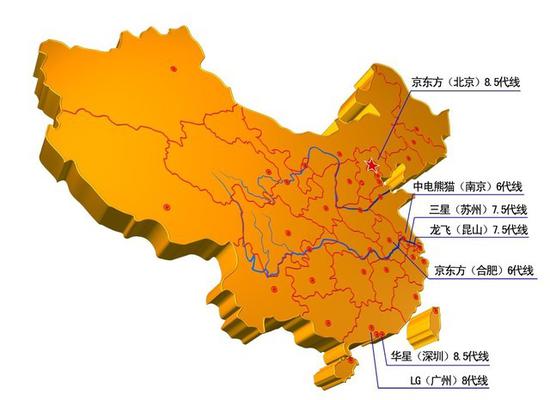

Part of China's domestic panel production line distribution

We must know that the panel industry was once the world of Japanese and Korean companies. Now that the size of the Mainland China has become the first, there are many reasons for this result. Some people think that China can achieve such a result, mainly because Japan and South Korea to give up the low-end panel industry, and concentrate on developing high-end display technology. The author believes that this idea actually lacks a comprehensive understanding of the Chinese panel industry.

Do foreign companies really have such goodness and let China’s panel industry take advantage of scale? Is China’s panel companies currently producing “low-end fruits†that people don’t want? With these questions, let’s take a look at the development of China’s panel industry. And the future.

What alms? Foreign companies are not so kind

In 2013, the National Development and Reform Commission sanctioned the price monopolies of six large international LCD panel makers from South Korea’s Samsung, LG, Chi Mei, Taiwan’s Chi Mei, AUO, Chunghwa Picture Tubes and HannStar’s Crystals from 2001 to 2006. A total of 53 private meetings were held by 6 overseas companies. The panel’s output, quantity, price, and related technical information have reached the same pace for the mainland sales panel.

In addition, these panel companies have also manipulated the panel prices of the US market. It can be seen that the so-called low-end panels do not exist, as long as you do not have this industry, as long as there is no competitor in this market, then even the most basic amorphous silicon LCD panels, It can also be used to get huge profits.

In fact, the world's panel industry is changing. Japanese panel companies made successive mistakes. Panasonic and other companies have failed to bet on plasma, and Japanese panel companies are suspicious of the expansion of Korean panel industry capacity. It was precisely because of the rise of the low-price panel in Korea that Japan’s vocal performance in this important market in China has been weakened.

At present, the Japanese display company has taken the joint road. JDI has been integrated into the display business of Toshiba, Sony, and Hitachi.

Although Japan used to be the overlord of the panel market, Japan's natural market is not large enough. Therefore, it must compete in the global market. Due to the blunder of strategy, the Japanese panel industry lost the opportunity to build a large-scale advantage. At present, we can only hope for technological advantages, so that we can once again gain monopoly status.

With the development of Japanese panel companies being frustrated, the panel industry has grown stronger in Korea. In fact, the predicament faced by South Korea is similar to Japan. The size of Korea’s own market cannot support the development of this market. However, South Korea has used the price advantages brought by scale advantages to enter the world market. Thus laid the South Korean panel for nearly a decade of glory.

What is interesting is that the Korean panel companies have followed the same path as the Chinese panel companies. They learned technology from high prices and then finally entered the market with low-priced products. Typical. Now China's new apprentice is rising. However, this is not Japan and South Korea's initiative to give up its scale advantage. Japan and South Korea face competitors like China, and they have no way to gain an advantage in terms of scale. They continue to struggle with China's PK scale, so they can only hope to suppress China in technology and thus take profits from top markets.

Three characteristics why the panel industry settled in China

So why is China's panel industry able to take its own path in the environment of strong rivals? We must analyze the basic characteristics of the panel industry. The LCD panel industry is a technology-intensive, capital-intensive, and labor-intensive industry. It is difficult to support the rapid development of the panel industry with only funds or technology alone. In the past, the panel industry in China was difficult to develop. The problem of capital shortage was not fundamental. The most important thing was that the technical foundation was too weak.

At the beginning of the new millennium, the failure of Chinese companies to try in the panel industry was a lack of technology. After 2008, China began to embark on the road of “reintroduction and reabsorptionâ€. Enterprises no longer rely on the purchase of outdated industrial lines as a core development method. While purchasing behind-the-line production lines, Chinese companies pay high-paying talents and continue to exert technical force. It can be said that the 10 years between 2008 and 2018 are the initial stages of China's panel industry technology.

At the same time, the panel industry is a capital-intensive industry, there is no large-scale capital investment, in the panel industry can not play. Capital intensive does not mean that there is money, which requires the government's strong support. The panel industry needs a lot of land. However, if the government does not support the acquisition of land, or if it increases the cost of acquiring land, it is clear that any panel company is faced with such a difficult situation. For example, the sixth-generation flexible AMOLED production line of BOE (BOE) Mianyang has a total investment of 46.5 billion yuan, covers an area of ​​1200 acres and has a building area of ​​700,000 square meters. Meanwhile, BOE (BOE) 8.5-generation new semiconductor display device production line in Fuzhou, the total Investment has also reached 30 billion yuan.

At the same time, the panel needs a lot of labor, and the knowledge level of the labor force must be guaranteed. The economic development of Chinese society in the last ten years can precisely provide such a labor force. Its cost is low and its level of knowledge is continuously improving. This is something that markets such as Southeast Asia cannot provide.

The development of China's panel industry is inseparable from the rapid rise of the national economy. This is the most solid foundation. However, with backing, no goal is also impossible. The Chinese government’s policy support, the growing demand in the Chinese market and the development of technology in the panel industry work together, so we have the scale of the status quo of the Chinese panel industry.

Policy and Market Counterattack of China's Panel Industry

In addition to the three major features of the Chinese market that are consistent with the development of the panel industry, it is also very important that the Chinese government's policies support this. First of all, in addition to the support on the land, Chinese financial companies’ support for panel companies is also an important reason. After all, to obtain such a large investment, without the power of the capital market, relying solely on production and profitability cannot be turned in the early stages. The period from the construction of the panel production line to profitability is three to five years, and the profitability during this period is very weak.

In the past, due to the high dependence on imports, China's import tariff on LCD panels was relatively low, and it was set at 3% in 2005. With the rise of China's panel companies, China’s panel import tariffs have risen to 5% in 2012. Currently, different tariff rates are implemented according to different generations of lines (2012 stipulates that 32-inch and higher LCD TVs do not include backlight module tariffs). The preliminary tentative 3% will be increased to 5%. According to the announcement of the Customs General Administration of the People's Republic of China Notice No. 65 of 2017 on the 2018 Tariff Adjustment Plan, the current liquid crystal glass substrates are not included in 6 generations (1850mm x 1500mm) or more. The tax rate is 4%, while the liquid crystal glass substrate 6 generation (1850mm × 1500mm) and the following tax rate of 6%, click to view the policy). This approach has increased the cost of foreign panel companies entering the Chinese market.

In addition to the government, the market is also an important part of the promotion of Chinese panel companies. Since 2008, China’s consumer demand for display products has continued to grow. From small mobile phones to large home flat screen TVs and commercial display screens, displays are beginning to become ubiquitous. To meet such a large number of display requirements, the panel is the most basic requirement. Although LED large screens and projection products can also meet some of the requirements, panel technology is still the most widely used technology.

Especially in the past few years, China has begun to show a trend of consumption upgrade. For the digestion of high-end products such as 4K TV, China is already well-deserved NO.1. The data from the China Electronics Video Industry Association shows that by the end of 2018, China's 4K TV penetration rate will reach 58%. The penetration of global 4K TV is still at a 30% level. This shows that China's market acceptance of the latest display technology is leading the world.

How to make the competition more violent

Having said so much about the advantages of China's panel industry, can China really sit back and relax? From the current world situation, the panel industry has been concentrated in East Asia. There are not many regions that can meet the development of the panel industry. It is obviously not easy for other regions to want to have the original accumulation. The labor costs in Europe and the United States are too high to have a price advantage. The labor costs in Southeast Asia are low, but there is a lack of technical support. India is a region with potential, which is worth noting.

At the same time, China’s panel industry also has its own shortcomings. The first is that technology cannot compete with the first tier. Therefore, Chinese panel companies must ensure innovation; the second is the relatively weak upstream power of Chinese panel companies, such as liquid crystal materials and polarizers. The production of such components does not yet have a complete industrial chain. Therefore, at a deep level, the prices of panel companies in China are still not fully autonomous.

With China's economic and social development, the original advantages of China's panel industry are also changing. For example, labor costs are no longer an advantage in the Chinese market. At the same time, due to the narrowing of the gap between advanced technology and Chinese companies, Chinese panel companies can no longer make progress through learning. In the future, they need to rely on their own research and development. This point, China's panel companies are not fully prepared.

In addition, the author believes that there is a greater risk that many Chinese panel companies are single companies. It is not like Samsung is a large-scale complex. In this way, the anti-risk capability of Chinese panel companies is relatively weak, and the cost of trial and error is too high. Samsung is a highly integrated representative of the industry chain. At present, Chinese enterprises have a decentralized layout and lack of alliances. They have no way to form a national or regional power system, and therefore they cannot establish the right to speak and pricing.

Of course, comprehensively, the advantages of Chinese panel companies outweigh the disadvantages, although some people say that the panel production in China is already too large. However, output is currently the only killer of the Chinese panel industry. If we automatically reduce production, the author thinks this is "self-respecting martial arts." It is clear that the timing for controlling production has not arrived yet. At the same time, Chinese panel companies cannot blindly focus on the domestic market. They need to form a coalition to actively participate in the competition in the global market and prepare for the transition of the panel industry. Although presently China has become one of the core areas of the panel industry, at present, it is mainly winning by quantity, large but not strong, insisting on independent innovation and forming alliances, and actively participating in the competition in the international market. I believe this is China. The vision of the panel industry

Solar home energy storage power supply

SHENZHEN CHONDEKUAI TECHNOLOGY CO.LTD , https://www.szsiheyi.com